Author – Joe Turkal, LtCol (Ret) USMC

For former military aviators transitioning into commercial airline careers, compensation has reached levels that rival or exceed many traditionally high-income professions. Widebody captains earning $400,000–$600,000+, combined with some of the most generous employer retirement contributions in the private sector, create the appearance of a highly optimized financial system but that appearance is misleading. The reality is that airline compensation has outpaced the retirement system’s design constraints, and the industry has only partially adapted.

What pilots encounter is not a lack of benefits, but a set of structural limitations imposed by tax law and plan design. These limitations directly affect how much can be saved and how efficiently those savings are taxed over time.

The most relevant financial planning issues are those driven by legal or plan-based constraints on retirement and tax savings. These are not behavioral issues. They are system constraints and four stand above the rest:

- The total contribution cap

- The compensation cap on eligible earnings

- Structural overconcentration in pre-tax assets

- The missing piece, non-qualified deferred compensation (NQDC) plans

Before I provide a technical description of the relevant financial planning issues for commercial airline pilots, especially former military pilots, consider the following vignette to illustrate the points that follow:

A Pilot’s Story: How Structural Limits Shape Retirement Outcomes (And Why Timing Matters More Than Most Realize)

John spent 23 years in the U.S. Air Force.

Like many pilots, his career was defined by discipline, consistency, and a clear progression of milestones. By the time he retired from active duty in his mid-40s, he had built a strong foundation; a military pension, a habit of saving, and a skill set that translated directly into a second career.

Within months, he was hired by a major airline. At the time, it felt like a continuation, not a transition.

Age 45–50: The Second Career Begins

John entered the airline at age 45. The pay was solid from the start, but what stood out most to him wasn’t the salary; it was the airline’s non-elective retirement contribution of eighteen percent.

That number stuck with him. Compared to what he had seen before, it felt exceptional. More importantly, it felt simple. The airline was doing most of the heavy lifting. In those early years, his focus was straightforward:

- Learn the system

- Upgrade as quickly as possible

- Save aggressively

By year four, he upgraded to Captain. His income increased significantly, and with it came a sense of financial confidence. He did what most high earners are told to do, which was to max out his 401(k) contributions as early as possible each year.

That approach was reinforced by his tax professional, who consistently advised him to prioritize pre-tax contributions to reduce his current taxable income. The logic made sense because his income was high, his tax bracket was high, and reducing taxable income today felt like an immediate win. It was clean, simple, and measurable.

So, John followed that advice year after year, contributing as much as possible, as early as possible, all on a pre-tax basis. It felt efficient, disciplined, and optimized. It wasn’t until later he realized it was none of these.

Age 50–55: The First Constraint Appears (But Isn’t Recognized)

By his early 50s, John was earning well into the high six figures. His mindset hadn’t changed and he continued to max out his contributions early each year, assuming he was doing exactly what he should be doing.

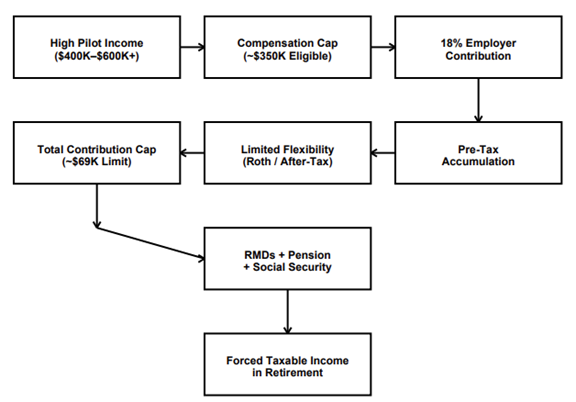

What he didn’t realize was that his plan had a limit, and not just on what he could contribute, but on how much he could contribute. The IRS caps total annual contributions to defined contribution plans. That cap includes both his contributions and the airline’s contributions.

As his income grew, the airline’s 18% contribution alone consumed most of that limit. John’s early-year contributions, combined with the airline’s ongoing contributions, began to press against that ceiling. At no point did anyone clearly explain the implication:

By aggressively contributing his own dollars, especially entirely on a pre-tax basis, he risked interfering with how the airline’s “free” contribution was ultimately credited, while simultaneously increasing his long-term tax exposure.

John did not realize that due to his high income; by maxing out his annual employee 401(k) contribution, he was crowding out the room for the airline to contribute the full 18% on his behalf. John missed out on many years of airline contributions before he realized that the IRS contribution cap combined with his max contribution reduced the airline’s contribution leaving “free money” on the table for years.

So, while his income continued to rise, his contribution base stopped growing and his effective contribution rate began to decline. The system plateaued, and at the same time, he continued following the same tax strategy of maximizing pre-tax contributions, reducing current taxable income, and deferring taxes into the future

From a year-by-year perspective, it worked, but, from a lifetime perspective, it was quietly building a large and growing concentration of pre-tax assets that would eventually be fully taxable.

Age 60–65: The System Looks Successful

At retirement, John did what most would consider everything right. He had a military pension, a large 401(k) balance, strong earnings history, and no major financial missteps. From the outside, his situation looked ideal.

He retired from the airline after 20 years, at age 65, confident that he had built more than enough retirement savings and fixed income. At this stage, there was no visible problem, but this is also where the third constraint begins to take shape.

Age 65–73: The Window That Went Unused

In the years immediately following retirement, John’s income dropped, but not as much as he expected. His military pension continued. He began drawing Social Security. His retirement accounts, primarily pre-tax, remained untouched.

This period represented something important, though he didn’t recognize it at the time. It was the most flexible tax window he would have for the rest of his life. He could have:

- Gradually shifted money from pre-tax to Roth

- Managed his tax brackets intentionally

- Reduced the future burden of required distributions

But his mindset had been shaped over decades. “Defer taxes. Reduce income now. Pay later.” So, he waited. He didn’t feel urgency. His accounts were growing. His income needs were met. There was no immediate pressure to act.

Age 73–75: The Constraint Becomes a Reality

At age 73, the system changed. Required Minimum Distributions (RMDs) began. Unlike previous decisions, this one wasn’t optional. The IRS required him to begin withdrawing from his retirement accounts, and those withdrawals were fully taxable.

What John hadn’t fully appreciated was how all of his income sources would interact: his military pension, his Social Security income, his RMDs from a large pre-tax portfolio. Each of these, individually, was manageable, but together, they created a concentrated stream of taxable income that he could no longer control.

His tax bracket increased. His Medicare premiums rose due to Income-Related Monthly Adjustment Amount (IRMAA) thresholds. A larger portion of his Social Security became taxable. And most frustratingly, he realized that the strategy that had reduced his taxes for decades had simply shifted and amplified them later in life.

Age 75: Looking Back

At 75, John wasn’t in financial trouble. But he was frustrated. Not because he had done anything wrong, but because he had followed advice that was incomplete. His tax professional had been correct in the short term. Reducing taxable income during peak earning years is often sound advice. But what John lacked was a coordinated strategy that considered contribution limits, income caps, and the long-term impact of accumulating primarily pre-tax assets.

If he could go back, the changes would not be dramatic. They would be deliberate. He would have:

- Coordinated his contributions to fully capture employer benefits

- Recognized that not all income participates equally in retirement plans

- Balanced pre-tax and after-tax savings earlier

- Used his early retirement years to reduce future tax exposure

Not because he lacked resources, but because he had options then that he no longer has now. {End of Vignette}

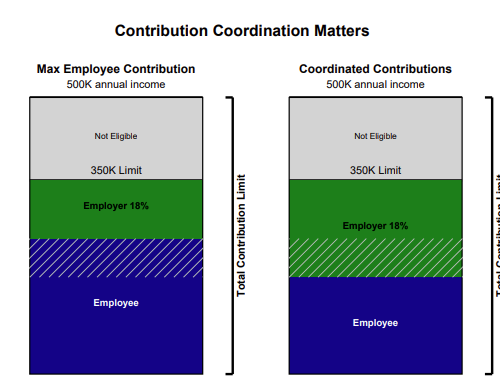

1. The Total Contribution Cap

Airline retirement plans are, by any objective measure, generous. Employer contributions of roughly 18% of pay are difficult to match elsewhere in the private sector. However, that generosity exists within a hard boundary: the IRS limit on total contributions to defined contribution plans. For 2026, that limit sits around $69,000 (excluding certain catch-up contributions), and it includes both employer and employee contributions.

At moderate incomes, this is not an issue. At higher incomes, it becomes binding very quickly.

A pilot earning $350,000 (increased to $360,000 in 2026) will see an employer contribution of approximately $63,000. At that point, only a small amount of remaining contribution capacity exists before the legal limit is reached. The system, therefore, begins to restrict the pilot’s ability to contribute independently. What appears to be a highly favorable structure begins to impose a tradeoff of more employer contribution, requires personal contribution control.

This constraint creates a subtle but important coordination problem, one that many pilots do not realize until after the fact. It is common for a pilot to take the standard approach of “maxing out” their 401(k) contributions as early as possible in the year. In some industries, that is sound advice. In the airline system, however, that approach can backfire.

Because total contributions are capped, aggressively contributing employee deferrals without accounting for the employer’s 18% contribution can interfere with how those employer dollars are ultimately credited.

Depending on how the specific plan operates, this can lead to:

- Employer contributions being limited during the year

- Adjustments or caps applied in real time

- Timing mismatches that affect how contributions are allocated

Even in plans with reconciliation features, the structure and timing may not perfectly align with the pilot’s expectations. The key insight is simple but not intuitive: Maximizing your personal contribution is not always the same as maximizing your total benefit. Proper planning requires coordination, not just participation.

Airlines have begun to recognize this issue and, in some cases, have implemented additional plan structures such as market-based cash balance plans to capture contributions that would otherwise be lost. These solutions help preserve total savings but do not meaningfully expand flexibility. They operate within the same tax-qualified framework and do not change the underlying constraint.

2. The Compensation Cap: The Hidden Ceiling on “18%”

While most pilots understand that contributions are limited, fewer recognize that income itself is also capped for retirement plan purposes.

Under current tax law, only compensation up to a specified threshold (approximately $350,000 in 2025, indexed annually) can be used to calculate retirement contributions.

This means that once income exceeds that threshold, the effective contribution rate begins to decline. A pilot earning $500,000 may assume they are receiving an 18% contribution across their full income. In reality, that percentage applies only to the capped portion of compensation. The result is a quiet but meaningful shift, where the stated contribution rate remains unchanged, but the effective contribution rate declines as income rises.

Over time, this creates a structural limitation on how much high pilots can accumulate in tax-advantaged accounts.

The system does not scale with income; it plateaus.

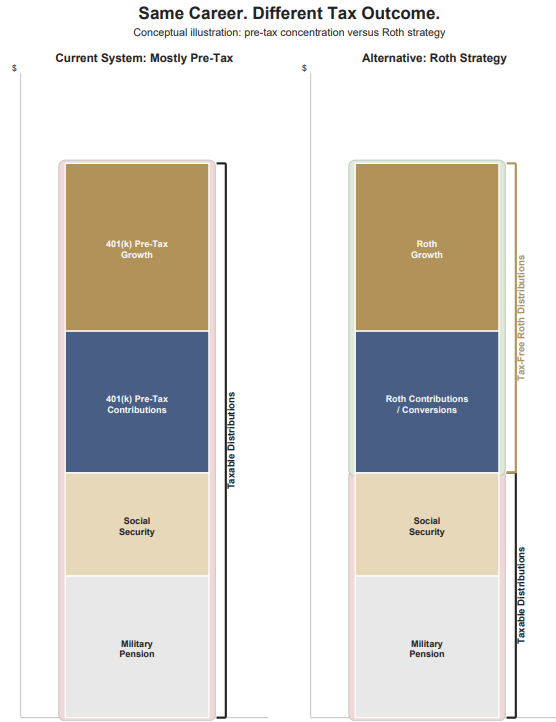

3. Pre-Tax Concentration and the Forced Tax Back

The first two constraints determine how money enters the system. The third determines how it leaves, or in other words, how it is withdrawn from the system

Airline retirement structures, when combined with military benefits, create a strong and persistent bias toward pre-tax accumulation. This bias is often reinforced by well-intentioned tax advice during peak earning years. Pilots typically build wealth across several sources:

- Employer retirement contributions (pre-tax)

- Employee contributions (often constrained in flexibility)

- Military pension (fully taxable)

- Future Social Security income

At the same time, many pilots, particularly during their highest earning years, are advised by their tax professionals to prioritize pre-tax contributions. The reasoning is straightforward, current income is high, marginal tax rates are high, and thus reducing taxable income in the present provides an immediate and measurable benefit of lower taxes. From a year-by-year perspective, this advice is often correct. However, when applied consistently over a full career, especially within the constraints of airline retirement systems, it can lead to a different outcome.

A growing concentration of assets and income streams that will all be taxed later, often at the same time. Individually, each source of income is valuable. Collectively, they create a concentration of future taxable income, sometimes referred to as a “tax bomb”.

This becomes most visible later in life, when Required Minimum Distributions (RMDs) begin. At that point, the system no longer allows for full discretion, income must be taken(from pre-tax funds, but not Roth), and it is taxed accordingly.

For many pilots, this results in:

- Mandatory income layered on top of pension income

- Higher tax brackets than anticipated

- Increased Medicare premiums due to IRMAA thresholds

- Greater taxation of Social Security benefits

What began as a strategy to reduce taxes in the present often results in higher total taxes paid over a lifetime, along with reduced flexibility in managing income. In effect, tax deferral in the present when overused, becomes tax compression in the future. For the majority of Americans in retirement, this strategy works because their tax bracket in retirement drastically reduces. But for those with high fixed income in retirement due to a military pension, the tax bracket in retirement stays the same or nearly the same. This, combine with RMDs, creates a “tax bomb” that is structurally in place for the remainder of life and results in potentially hundreds of thousands of extra dollars paid in tax over a lifetime.

A Visual: How the Constraints Interact

Below is a simplified view of how income flows through the system and where constraints are applied:

Next is a graphic describing two strategies, one employed by John in the earlier vignette and the second by a pilot receiving professional advice.

4. The Missing Piece: Why Other Industries Look Differently

In other high-income professions (e.g. executive roles), these constraints are not new, and they are often addressed more directly. Many companies provide access to non-qualified deferred compensation (NQDC) plans, which allow individuals to defer income beyond qualified plan limits and better control the timing of taxation.

The airline industry has begun to move in this direction, but not consistently. Of the top three U.S. airlines one has implemented a pilot-accessible NQDC plan beginning in 2026, one includes provisions allowing for such plans, but not as a broadly implemented standard, and one has focused primarily on qualified-plan solutions. The takeaway is not that airlines are ignoring the issue, but that the response remains incomplete and uneven.

Former military pilots entering commercial aviation are in a position of financial strength, but also one of structural complexity. The system delivers high income and strong benefits, but it also imposes limits that cap how much can be contributed, limit how much income can participate, and concentrates taxation into future years. These are not flaws, they are constraints, and constraints require planning. The airline industry has built a powerful compensation system, but one that operates within IRS rules it does not control, and so far, has adapted inadequately. Understanding those rules and planning around them is what separates a good outcome from an optimized one. John went on to have a great, well-funded retirement, but ultimately regretted not seeking a financial professional along the way. He endured vivid reminders every month when he paid the highest premiums on social security, was terminally stuck in the 32% tax bracket after age 73 and had to pay higher taxes on his social security every year.